Search

Search

- Propose energy development strategies in stages to provide reference for ASEAN's green transformation

- The report provides a multidimensional analysis of the energy situation in Southeast Asia, clearly highlighting the multiple shortcomings in regional development

The ongoing geopolitical conflict in the Middle East continues to stir up the global oil and gas market, and Southeast Asia, located between energy supply and demand, is facing multiple challenges such as a surge in energy consumption, increased pressure to reduce emissions, and high dependence on foreign energy. This region, which is rich in scenery, geothermal energy, and key mineral resources, is facing a rapid expansion of electricity demand for industrial, refrigeration, and digital industries, as well as insufficient investment in clean energy and weak disaster resistance of energy infrastructure. The opportunities and challenges of the transformation path are intertwined.

Recently, the International Energy Agency released the seventh edition of the Southeast Asian Energy Special Report, which takes the Middle East geopolitical energy crisis as the starting point, divides three policy scenarios to compare energy development differences, and provides authoritative references for regional energy security and low-carbon transformation.

Regional Energy Status and Shortcomings

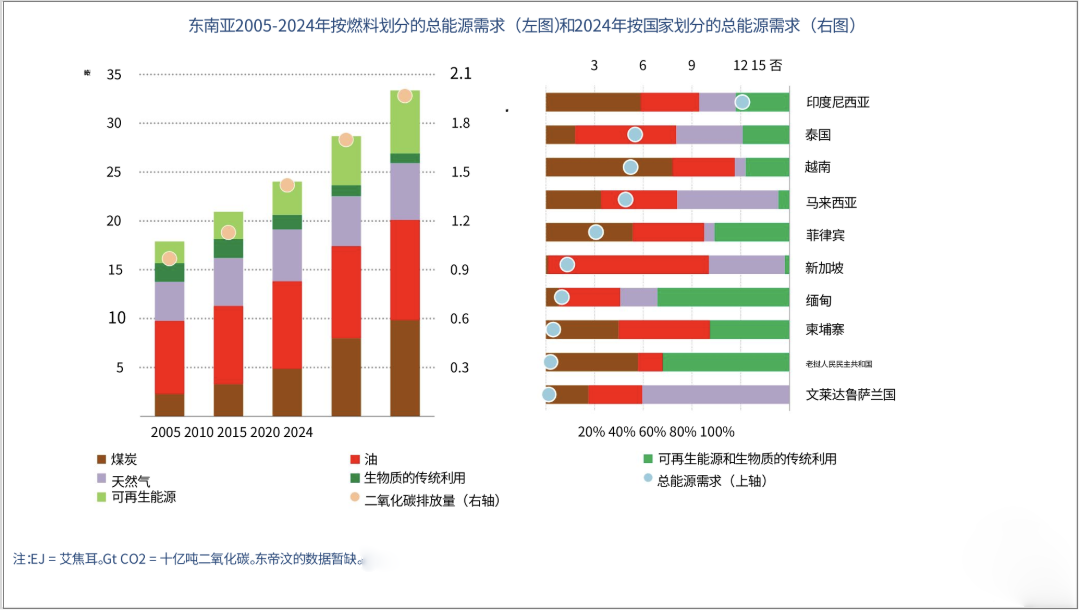

Southeast Asia's energy demand continues to rise, with a high proportion of fossil fuels; There are abundant reserves of scenery and rare mineral resources, but there is insufficient investment in clean energy, uneven access to energy, and weak resilience of energy infrastructure to climate disasters. The volume of energy demand continues to expand, with a structural emphasis on fossil fuels. Southeast Asia accounts for about 9% of the global population, economic size, and energy consumption, with a relatively high energy intensity. From 2015 to 2024, the cumulative energy consumption in the region will increase by 40%, and the average annual increase in carbon emissions will be 4%. Coal is the main source of energy consumption increase, and although the growth rate of wind and solar power has reached 35%, the base is too low and the substitution effect is limited.

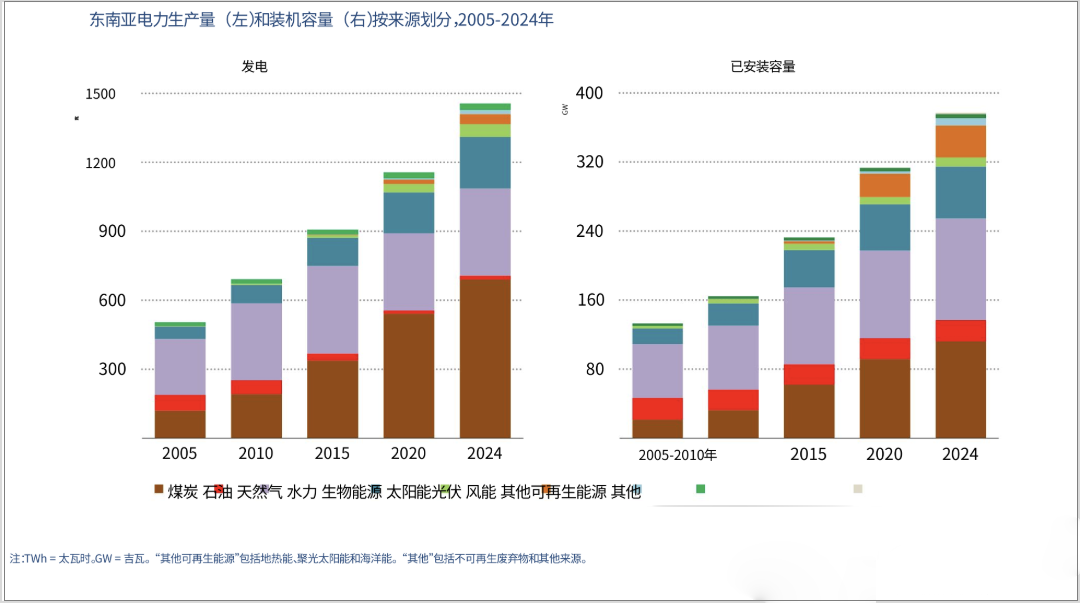

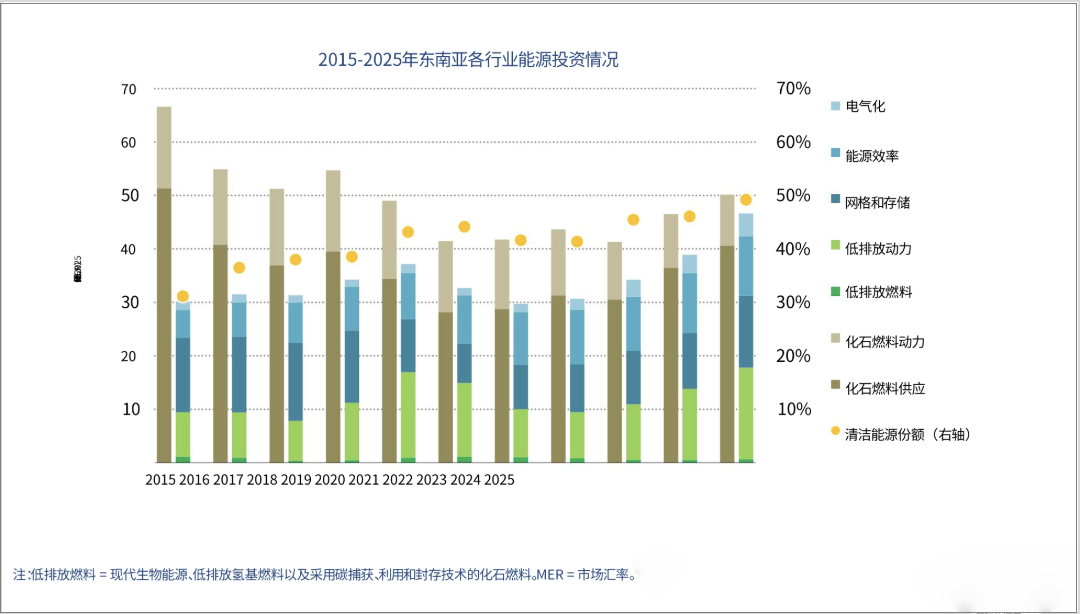

In 2024, the regional terminal energy consumption will be 21 joules, with industry, transportation, and buildings ranking among the top three energy consumption scenarios; Oil accounts for nearly half of terminal consumption, with industrial electricity mostly coming from nickel metal smelting, transportation consuming more than half of oil, and the potential for growth in electricity consumption for cooling in tropical buildings is enormous. In the same year, the total power generation in the region was 1457 terawatts, with coal-fired and gas-fired power as the main sources, and wind and solar power accounting for only 4%; The growth rate of electricity demand is twice that of overall energy consumption, and data centers are further increasing their electricity load. The endowment of clean energy resources is outstanding, but there are obvious shortcomings in industrialization and investment. The region has abundant resources in terms of scenery, hydropower, and geothermal energy, with globally leading reserves of key new energy minerals such as nickel and rare earths. There are three major pain points in industrial development: dependence on imports from the Middle East for nickel smelting raw materials, and facing overseas trade barriers for photovoltaic exports; The global investment in clean energy accounts for only 3%, with insufficient investment in power grids and energy storage; The supporting facilities of the upstream and downstream industrial chain of new energy are not perfect.

Energy accessibility and climate risks, uneven development, and weak resilience to risks. The region has basically achieved electrification, but 120 million people lack clean cooking fuels, and most people rely on liquefied petroleum gas; Nearly 20% of thermal power and photovoltaic facilities are located in high-risk flood prone areas, and energy facilities in many countries are susceptible to damage from floods and cyclones, resulting in poor system resilience.

Predicting the trend of transformation in three types of scenarios

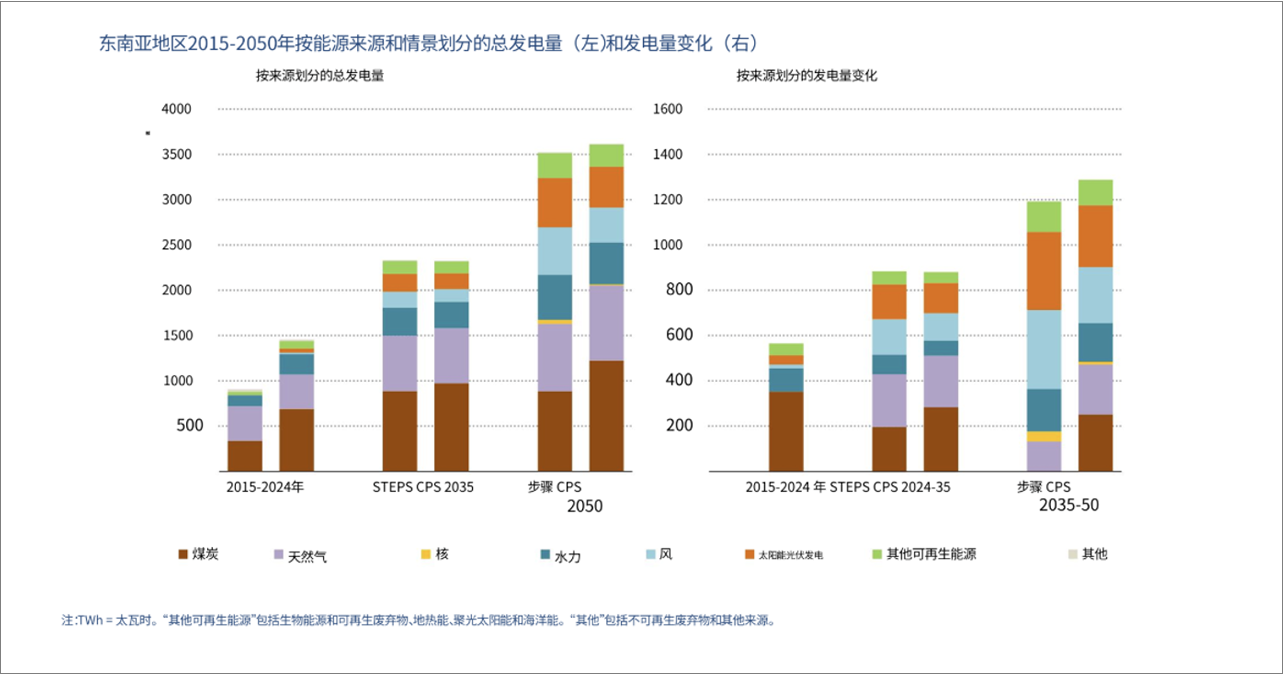

The report sets three policy paths to calculate the energy outlook from 2035 to 2050, and the greater the policy implementation, the more prominent the regional decarbonization effect. The total energy demand and carbon emissions, as well as the degree of policy implementation, determine the effectiveness of the transformation.

Current policy scenario: Energy consumption and carbon emissions continue to rise, with fossil fuels accounting for 72% by 2050, and the transition is almost stagnant.

Established policy scenario: The growth rate of energy consumption slows down, clean energy accounts for 40% of the new energy consumption, and the upward trend of carbon emissions is under control.

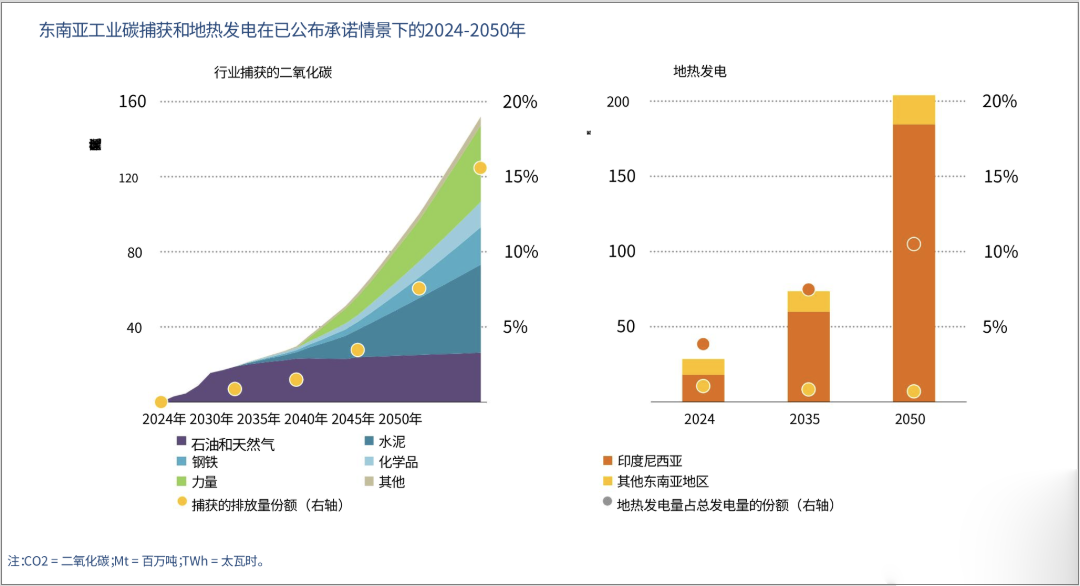

The commitment scenario has been announced: the transformation effect is optimal, carbon emissions will peak by 2030, and renewable energy and nuclear energy will account for 62% of primary energy by 2050.

New energy is gradually replacing fossil fuels as the main power source. Under current policies, coal-fired power will continue to dominate electricity supply by 2050; Implement existing policies and increase the proportion of clean energy generation to 43%; After fully fulfilling the emission reduction commitments, the proportion of low-carbon power generation such as wind and solar power, nuclear power, and hydropower will reach 90%. It is necessary to significantly expand the power grid and add 300 gigawatts of energy storage to adapt to new energy consumption. Low carbon investment continues to expand, while fossil fuel investment is gradually shrinking. Only maintaining the current policies, energy investment still focuses on fossil fuels; After fully implementing emission reduction commitments, investment in low-carbon electricity and grid energy storage has significantly increased, while coal related investment continues to shrink.

Opportunities, Challenges, and Countermeasures

Sort out the implementation plans for low-carbon technologies such as wind and solar power, nuclear power, and energy storage, analyze the advantages and disadvantages of transformation, and provide a layered regulation plan in the short, medium, and long term. The implementation path of core low-carbon transformation technology focuses on wind and solar power, with geothermal hydropower as the backup. Photovoltaic wind power is the core of the transformation, and geothermal power supply can compensate for fluctuations in new energy. The space for hydropower development is becoming saturated. Nuclear power supplements low-carbon power supply, and many countries are planning to build new nuclear power plants. With the reduction of financing costs, competitiveness has significantly improved, which can significantly reduce coal consumption. Energy storage connects with cross-border power grids to overcome consumption bottlenecks, battery energy storage stabilizes wind and solar power output, and underwater DC transmission builds an ASEAN interconnected power grid to achieve cross-border power allocation. Regional collaborative hedging of supply risks, relying on cross-border routes to connect advantageous energy sources in various regions, joint reserve of oil and gas by multiple countries, and joint construction of emergency energy security mechanisms. Low carbon fuels and carbon sequestration technologies help with deep decarbonization, promote biofuels and green hydrogen, gradually build carbon capture facilities, and improve a diversified low-carbon energy system.

Major opportunities for energy transformation in Southeast Asia. One is to improve energy security, replace fossil fuel imports with clean energy, and alleviate the impact of geopolitical oil prices; Secondly, relying on mineral advantages to build a complete new energy industry chain, it is expected to become a global industrial cluster; Thirdly, the ASEAN energy integration mechanism disperses supply risks, and special financing reduces the construction costs of low-carbon projects. The four major structural core challenges. The dependence on geopolitical oil and gas imports is difficult to change in the short term, which drives up people's livelihood expenditures; The financing cost of low-carbon projects is much higher than that of developed countries; Coal power is the foundation for ensuring supply, and it is difficult to balance carbon reduction and stable power supply; The upstream and downstream industrial chains have a high degree of external dependence and are susceptible to external trade restrictions. Keywords:Foreign construction news network,Southeast Asia engineering information network,Overseas engineering construction,Foreign engineering construction news

To ensure short-term security and stability of people's livelihoods, increase strategic reserves of oil and gas, promote energy-saving measures, provide targeted subsidies to low-income groups, and optimize fossil energy subsidies. Medium - and long-term promotion of transformation and strengthening of the system, large-scale layout of wind, solar, and nuclear power, and construction of an ASEAN interconnected power grid; Improve the mineral deep processing industry chain, develop transformational finance and carbon trading; Promote clean energy use while balancing emissions reduction, supply guarantee, and people's livelihood development.Editor/Gong Ziwei

Comment

Praise

Praise

Collect

Collect

Comment

Comment

Share

Share

Write something~