Search

Search

- Chinese photovoltaic enterprises have fully landed overseas, completing the transformation of pure export

- Southeast Asia's photovoltaic increment continues to release, becoming a core growth region for global new energy

The scorching light at the equator is being cut and transformed at an unprecedented density, injecting into the industrial bloodline of the South Pacific Islands. In this arc-shaped area constructed by the Kuril Islands, sunshine is no longer just a footnote to climate, but has evolved into a core variable that reshapes the geopolitical energy landscape. The Chinese photovoltaic industry is taking this as an anchor point and undergoing a deep transition from commodity output to civilized form implantation.

Regional photovoltaics usher in a growth trend

In the past year, the photovoltaic industry in Southeast Asia has experienced rapid growth. The recovery of the Vietnamese market, the surge in module imports from the Philippines, and the launch of a 100GW photovoltaic plan in Indonesia have officially led to a surge in installed capacity for regional photovoltaics. By the end of 2025, the total installed capacity of photovoltaics in Southeast Asia will be 38.3GW. Chinese photovoltaic companies will no longer only export products, but have also implemented manufacturing, engineering general contracting, and energy storage supporting businesses throughout the entire industry chain. At the same time, they will also have to deal with multiple challenges such as policy changes, overseas tariffs, and local implementation.

Each of the five countries has its own unique market development characteristics

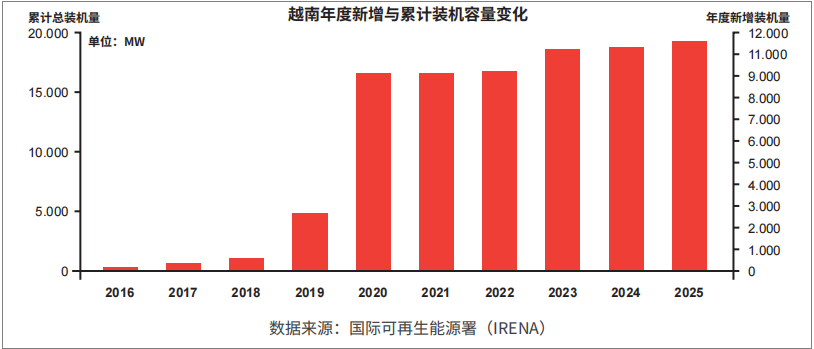

Vietnam's photovoltaic installed capacity of 19GW ranks first in Southeast Asia, with significant fluctuations in development. From 2019 to 2020, subsidies gave rise to a wave of installed capacity, with an increase of 11.6GW in 2020; from 2021 to 2024, subsidies were cancelled and the power grid was under pressure, causing the market to almost stagnate; In 2025, the new policy will be implemented, with a total of 586MW of new installed capacity added throughout the year. The new regulations will simplify the approval process for rooftop photovoltaics, increase long-term photovoltaic installation targets, and add mandatory requirements for energy storage facilities. Companies such as Longi, Tianhe, and Jinko have established factories locally, but the maximum 46% tariff in the United States has caused the projects to be put on hold, testing the comprehensive strength of the companies in the local market.

By 2025, the total installed capacity of photovoltaics in Thailand will be 3.9GW, with 87% being rooftop photovoltaics, resulting in a significant increase in the number of households with civilian installations. Multiple support policies have been introduced locally, including declaration of installation capacity, personal income tax reduction, low interest loans, and surplus electricity purchase. Jinko holds a 34% market share in Thailand and has deep cooperation with multiple domestic leaders. The high tariffs of up to 799.55% in the United States have suppressed local production capacity exports.

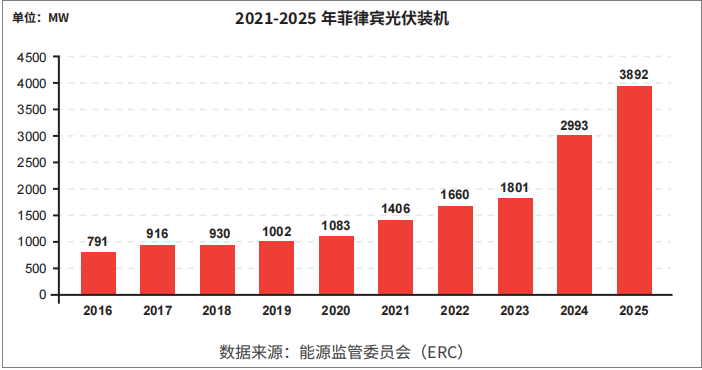

By 2025, the Philippines will have a photovoltaic installed capacity of 3.9GW, mainly consisting of large-scale ground power stations; By the first four months of 2026, China will import over 4GW of components, making it the top exporter of Chinese components in the Asia Pacific region. Multiple rounds of energy auctions have released over 10GW of photovoltaic projects, including floating photovoltaics and solar storage projects. Simplify the local approval process, increase subsidies for new energy, and provide favorable market development conditions. Longji has won the largest single photovoltaic power station in the local area, while China Energy Engineering and Electric Power Construction have undertaken a large number of projects, and Central Ring has laid out a local production base.

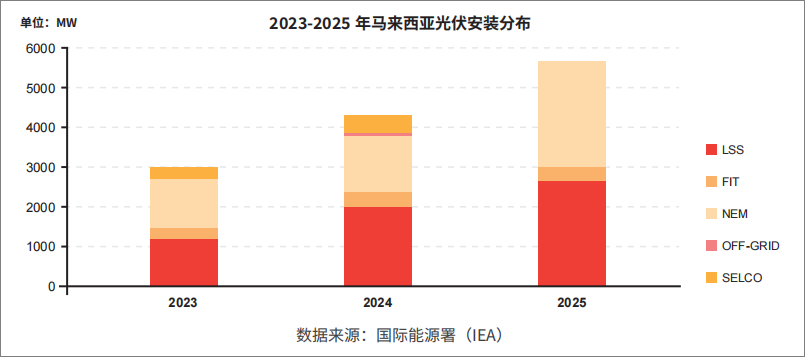

By 2025, Malaysia's photovoltaic installed capacity will be 5777MW, with an annual increase of 1448MW. With the support of three sets of policies including large-scale photovoltaic bidding, net metering, and grid electricity pricing, it will steadily expand. In 2026, the new photovoltaic policy will cancel the installation quota and provide cash subsidies for residential photovoltaic facilities to reduce installation costs. LONGi is building an integrated production line, with multiple companies laying out battery components; DeYe plans to invest 150 million US dollars in building a solar energy storage factory. The high tariffs imposed by the United States have blocked the export of local products to the United States, and foreign investment in power plant development is limited by a 49% shareholding limit, restricting development.

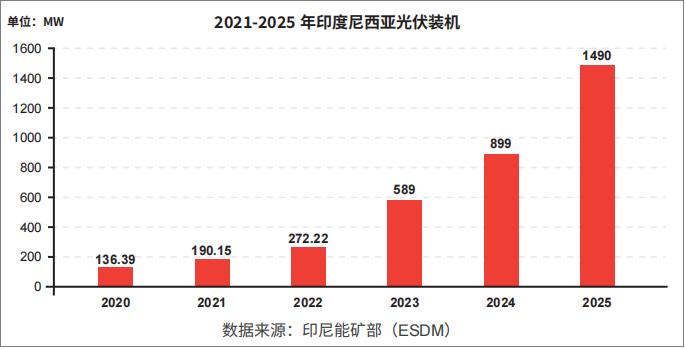

Indonesia is a global leader in solar energy resources with enormous potential for development, but its installed capacity will only be 1.49GW by the end of 2025. The local government has introduced a 100GW photovoltaic development plan, with renewable energy becoming the main source of new electricity, and industrial and commercial photovoltaics rapidly becoming popular. Longi, Tianhe, Hengdian Dongci, and Ningde Times have all landed large-scale photovoltaic and energy storage production projects. The US anti-dumping investigation has brought high tariffs, and the local certification process is cumbersome and costly, becoming an obstacle to foreign investment landing. Keywords: Southeast Asian photovoltaics, installed capacity growth, Chinese enterprises going global

Industry Summary and Insights for Going Global

The development stages of photovoltaics in the five Southeast Asian countries are different, and overall they rely on policy incentives to continuously increase installed capacity. Vietnam is steadily recovering, Thailand is deeply cultivating household photovoltaics, the Philippines has sufficient project reserves, Malaysia is running in parallel, and Indonesia is about to experience an industrial boom. For Chinese photovoltaic companies, Southeast Asia is a key overseas stronghold for the layout of the entire industry chain, technology output, and long-term operation.Editor/Gong Ziwei

Comment

Praise

Praise

Collect

Collect

Comment

Comment

Share

Share

Write something~